Definitive Guide · Real Assets & Digital Markets

From pilot programs to a projected $4 trillion market, tokenization is fundamentally reshaping how real property is owned, financed, and traded. This guide covers everything from asset types and deal structures to the risks that separate genuine opportunities from costly mistakes.

The Tokenization of

Real Estate Assets:

A Definitive Guide

PUBLISHED

March 2026

AUTHORS

Three Vectors Capital Research

READING TIME

18 Minutes

$4T

PROJECTED TOKENIZED RE BY 2035 (DELOITTE)

27%

CAGR 2024 - 2025 FORECAST

58%

REAL ESTATE FIRMS IMPLEMENTING OR PILOTING TOKENIZATION

$300B

ESTIMATED TOKENIZED RE MARKET 2024 (DELOITTE)

75%

GROWTH IN TOKENIZATION PLATFORMS GLOBALLY IN 2023

What Real Estate Tokenization Actually Means — and Why It Matters Now

Introduction

Real estate has long carried a paradox at its heart. It is the world's largest asset class with global real estate is estimated at more than $630 trillion in value yet it is also among the least accessible and least liquid. High minimum investment thresholds, opaque markets, sluggish settlement cycles that routinely span weeks or months, and the sheer indivisibility of a physical building have historically confined direct property ownership to wealthy individuals and large institutions.

Tokenization changes that calculus in a fundamental way. At its core, the process converts ownership rights in a real property asset or in a legal vehicle holding such an asset into digital tokens recorded on a blockchain. Each token represents a fractional, programmable claim on the underlying asset. Those tokens can be issued, transferred, and in some cases traded with a degree of speed, transparency, and automation that traditional real estate transactions simply cannot match.

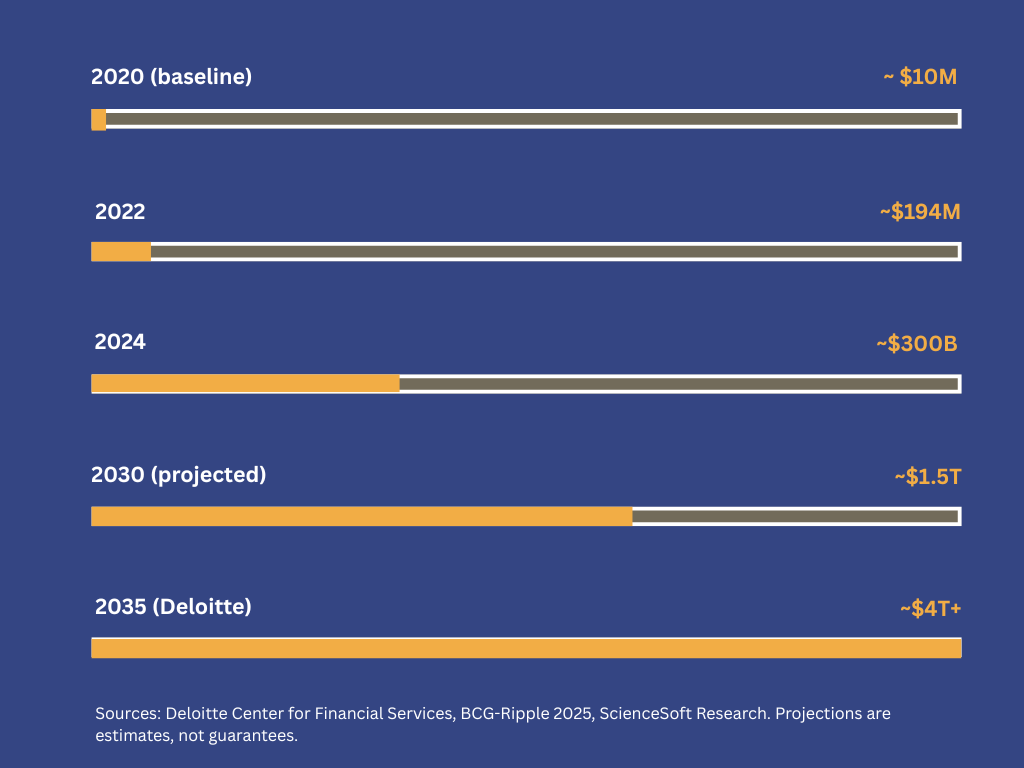

The concept is not new. The first significant tokenized real estate transaction was Elevated Returns' security token offering for the St. Regis Aspen Resort in Colorado which closed in 2018. But the market has moved from novelty to serious institutional consideration with striking speed. Deloitte's Center for Financial Services, one of the most cited voices on the topic, projects that tokenized real estate will grow from less than $300 billion in 2024 to over $4 trillion by 2035, representing a compound annual growth rate of 27%. Even the more conservative institutional estimates describe a multi-trillion-dollar transformation over the next decade.

What has changed is not merely the technology, blockchain infrastructure has been available for years. What has changed is the intersection of three forces: growing regulatory clarity in key jurisdictions, the credibility lent by major institutional participants (BlackRock, JPMorgan, KKR, Hamilton Lane), and the emergence of compliant, production-grade tokenization platforms that can handle the legal, custodial, and compliance requirements that institutional capital demands.

This guide provides a comprehensive, current, and practically oriented view of real estate tokenization as it stands in early 2026: what has been done, who is doing it, where the genuine opportunities lie, the real advantages it offers to different classes of participants, and the risks and pitfalls that separate thoughtful execution from costly failure.

“Every stock and bond would eventually live on a shared digital ledger. Tokenization is not a product — it is a new market structure.”

Larry Fink, CEO, BlackRock — January 2024

Which Real Estate Assets Have Been Tokenized?

ASSET TYPES

Tokenization is not confined to a single property type. The past several years have seen transactions spanning a wide spectrum of real estate assets, though adoption has been uneven and the maturity of tokenized offerings varies considerably by category.

Hospitality & Trophy Assets

The market's origin point. Elevated Returns' 2018 tokenization of equity in the St. Regis Aspen Resort raised $18 million and established the proof of concept. Tokens listed on the tZero secondary platform saw a 3.3x price appreciation through 2022–2024, demonstrating that investor appetite for branded, high-quality assets can persist through market cycles.

Residential & Multifamily

The highest-volume segment today, largely driven by retail-focused platforms. RealT has tokenized over $150 million in U.S. multifamily properties on Ethereum with tokens available from as little as $50, distributing daily stablecoin rental income. HoneyBricks (now EquityMultiple) closed $180 million in multifamily deals for over 3,500 investors in 2025. Lofty AI and similar platforms have made residential income properties accessible at near-micro-ticket sizes.

Commercial Real Estate

CRE tokenization is accelerating, particularly for office, industrial, and mixed-use assets. France and Japan have pursued tokenized commercial property debt structures. StegX and Zoniqx launched over $100 million in institutional CRE on the Hedera blockchain in 2025 targeting European and U.S. institutional investors. The CRE segment is drawing the most serious institutional attention as deal sizes align with institutional minimums.

Development & Construction Projects

Deloitte identifies tokenized ownership of under-construction and undeveloped land as one of three core pillars of the emerging tokenized RE ecosystem. Several Latin American and Asian developers have used tokenization to raise pre-construction capital, distributing risk and return across a broader investor base while gaining non-bank financing alternatives.

Private Real Estate Funds & REITS

KKR and Hamilton Lane have both tokenized fund interests via platforms like Securitize, opening access to qualified investors who previously could not meet traditional minimums. This fund-tokenization model is considered by Deloitte to be the largest near-term opportunity in the sector. Kin Capital launched a $100 million real estate debt fund on the Chintai blockchain in 2025, targeting qualified global institutional investors.

Real Estate Debt, Loans & Securitizations

Tokenized real estate debt instruments like mortgages, mezzanine loans, trust deeds represent a structurally important category. Smart contracts can automate interest distributions and repayment schedules, and tokenized debt can be used as programmable collateral in financial transactions. France has been particularly active in tokenizing commercial real estate debt within its MiCA-compliant framework.

The Legal Wrapper: What Is Actually Being Tokenized?

A critical technical and legal point that investors must understand: in virtually all real-world tokenization structures, you are not tokenizing the physical property itself or the land registry entry. You are tokenizing interests in a legal vehicle, typically a Special Purpose Vehicle (SPV), LLC, LP, or fund structure that holds the real estate. The token represents a fractional claim on that entity, which in turn holds the asset.

This distinction is consequential. The quality of the legal wrapper, its jurisdictional registration, and the enforceability of the link between the digital token and the underlying legal rights determine whether investors actually have a claim on the property or merely a contractual promise that a counterparty may or may not honor.

Case Study · Milestone Transaction

St. Regis Aspen Resort STO (2018)

Elevated Returns tokenized the equity of the luxury Colorado resort, raising $18 million from accredited investors under Regulation D. Tokens were listed on the tZero alternative trading system. The token price appreciated by 30% within 18 months of issuance and continued to a 3.3x gain through 2022–2024, trading strongly even through COVID-era uncertainty. The transaction remains the market's most-cited proof point not merely because it worked, but because it worked on a secondary market over multiple years, under real market conditions.

Who Are the Issuers and Investors?

MARKET PARTICIPANTS

The tokenized real estate market has evolved from a narrow ecosystem of crypto-native platforms and adventurous family offices into a broader, institutionally anchored marketplace. Understanding who is playing and what role they occupy is essential to understanding where the market is and where it is going.

Issuers: Who Is Bringing Assets to Market?

Real estate operators and asset managers are the primary issuers, either tokenizing single assets they own or creating tokenized fund structures that aggregate multiple properties. These range from boutique hospitality groups (Elevated Returns, St. Regis Aspen) to global asset managers. KKR, Hamilton Lane, and Apollo have all tokenized fund interests to broaden their capital formation reach.

Developer-issuers are increasingly using tokenization as a capital raising tool, particularly for projects in Latin America, Southeast Asia, and the Gulf states, where traditional bank financing may be costly or restrictive. Platforms like Brickken have facilitated residential and hospitality asset tokenizations across the region.

Real estate debt originators — mortgage lenders, mezzanine financiers, and trust deed lenders are tokenizing loan portfolios to create programmable, tradeable debt instruments. Kin Capital's $100 million real estate debt fund on Chintai is an institutional-grade example. DigiShares, operating across 40+ countries, processed $1 billion in securities by 2025.

Tokenization platforms acting as issuance infrastructure — Zoniqx, Tokeny, Securitize, RealT, SolidBlock, Polymath, and others provide the technical and compliance scaffolding for issuers, often taking an active role in structuring and distributing offerings. Securitize, in which BlackRock has invested $47 million, has become arguably the most influential institutional-grade platform globally.

Investors: Who Is Buying?

The investor base bifurcates sharply between institutional and retail, with very different motivations, minimum thresholds, and regulatory treatment.

Institutional investors — sovereign wealth funds, pension funds, family offices, hedge funds, and large asset managers are the fastest-growing segment by capital. Surveys show that 80% of high-net-worth investors and 67% of institutional investors already invest in or plan to invest in tokenized assets, with institutional allocations expected to reach 5–9% of portfolios by 2027. The motivation is primarily operational: faster settlement, automated compliance, 24/7 liquidity access, and programmable distributions represent genuine efficiency gains for institutions managing large, complex portfolios. J.P. Morgan's Onyx platform (formerly known via JPM Coin) has processed over $900 billion in tokenized transactions since inception and moved into live production with major buy-side firms in 2025.

Crypto-native institutions and DeFi protocols — Ondo Finance, MakerDAO, and others have emerged as significant buyers of tokenized real-world assets, using them as yield-bearing collateral in decentralized finance systems. Ondo Finance, backed by BlackRock, holds over $1.6 billion in tokenized assets and represents a genuinely new class of institutional investor that did not exist five years ago.

Accredited retail investors occupy a middle tier: individuals who qualify as accredited under Reg D (in the U.S.) or equivalent offshore frameworks, but who would not traditionally have access to institutional-grade real estate investments. Platforms like RealT, Lofty AI, and HoneyBricks target this cohort, offering tickets from $50 to $50,000 with automated rental income distributions.

Non-accredited retail investors remain largely excluded from U.S. tokenized real estate offerings due to SEC securities classification. In Singapore, parts of Europe, and the UAE, more permissive frameworks have allowed broader retail participation. This regulatory asymmetry is one of the most significant near-term constraints on the market's growth.

KEY INSIGHT -INSTITUTIONAL SIGNAL

The entry of BlackRock into tokenization is not merely symbolic. Its BUIDL fund, a tokenized U.S. Treasury product on Ethereum crossed $2.3 billion in TVL by mid-2025, capturing 45% of the tokenized treasury segment. BlackRock's $47 million investment in Securitize signals a deliberate strategy to own the infrastructure layer of institutional tokenization, including real estate. When the world's largest asset manager commits $47 million to tokenization infrastructure and builds a fund that crosses $2.3 billion in TVL within months, the signal is unambiguous: this is no longer an exploratory position. It is a strategic one.

MARKET POSITIONING

The Current Sweet Spot and the Road to Mainstream

Not all real estate assets are equally suited to tokenization at this stage of market development. Understanding where the genuine near-term opportunity lies as opposed to where the theoretical long-term opportunity exists is essential for both issuers and investors.

Where Tokenization Works Best Today

Assets with clear, stable cash flows are the most natural candidates. Rental income properties, income-producing commercial real estate, and real estate debt instruments all generate regular distributions that smart contracts can automate reliably. Tokenization adds the most unambiguous value when the underlying economics are straightforward and the primary friction is administrative — settlement, compliance tracking, distribution management.

Institutional-scale assets structured as funds represent the largest near-term opportunity, according to Deloitte's analysis. A tokenized fund that holds multiple properties allows institutional investors to gain diversified exposure with significantly lower minimum investments, automated redemption mechanics, and on-chain cap table management. This structure aligns best with existing securities frameworks in the U.S. (Reg D), EU (MiFID II / AIFMD), and Singapore (MAS frameworks).

Cross-border transactions are a compelling use case that traditional real estate market infrastructure handles poorly. A Japanese pension fund investing in U.S. commercial real estate through a tokenized structure faces far fewer settlement, custody, and administrative frictions than through traditional channels. Several 2025 transactions involving Middle Eastern sovereign capital accessing European and U.S. properties through tokenized vehicles underline this cross-border premium.

Deal sizes in the $10–250 million range currently represent the sweet spot. Smaller deals struggle to absorb the legal, compliance, and technology setup costs (which can run $150,000–$500,000+ for a properly structured offering). Larger deals are beginning to attract institutional attention but require more sophisticated multi-jurisdiction compliance architecture. The $10–250 million range offers enough scale to justify the setup investment while remaining manageable for mid-market institutional investors and family offices.

The Infrastructure Maturing in Real Time

Several developments in 2024–2025 have materially accelerated the market's institutional readiness. The EU's MiCA regulation, fully applicable since December 2024, provides clear legal treatment for tokenized assets across the single market. Dubai published dedicated real estate tokenization rules in mid-2025. Singapore's MAS and Hong Kong's SFC have both established sandbox and licensing frameworks that enable compliant tokenized real estate activity. Luxembourg's Blockchain Law IV, passed in December 2024, strengthened legal foundations for blockchain-based securities management.

In the U.S., the regulatory posture has shifted meaningfully since early 2025. The Trump administration's January 2025 executive order on digital financial technology, the Genius Act providing stablecoin clarity, and a more receptive SEC posture have collectively reduced the legal uncertainty that had been the single largest institutional barrier. Bank of America, Citi, and Coinbase are now actively exploring tokenization products under this changed regime.

On the infrastructure side, Swift's partnership with Chainlink and major global banks — BNY Mellon, BNP Paribas, Citi, Lloyds Banking Group to enable cross-network transfer of tokenized assets is laying the interoperability rails that the market has long needed. Today, tokens are still largely traded within the platform of issuance, severely limiting secondary market liquidity. The Swift/Chainlink initiative, once operational, could transform this constraint fundamentally.

"Tokenization is not just about fractionalizing trophy assets. It is about shortening settlement cycles, freeing trapped collateral, and creating programmable market infrastructure."

Zoniqx · Institutional Tokenization Report, 2025

VALUE PROPOSITION

The Advantages of Tokenization — For Whom, and Why?

Tokenization's advantages are real but they are not uniformly distributed across all participants. The benefits to an institutional asset manager differ materially from those to a retail investor or a property owner seeking capital. Clarity on this is important; much of the marketing rhetoric around tokenization obscures genuine distinctions.

For Asset Owners and Issuers

Property owners and fund managers have the most to gain in the near term from tokenization, across three primary dimensions.

Expanded and diversified capital access. A tokenized offering can reach a global pool of qualified investors simultaneously, reducing dependence on a handful of relationships or local capital markets. Elevated Returns' $18 million Aspen raise completed in a fraction of the time a traditional syndication would require, demonstrated this vividly. For assets in markets with shallow local capital pools, the ability to access cross-border capital at scale is transformative.

Lower issuance and administration costs over time. Smart contracts automate distributions, corporate actions, investor notifications, and compliance enforcement. While the upfront technology and legal costs are substantial, the ongoing operational savings, particularly for assets with many fractional owners, can be significant. Estimates suggest administrative cost reductions of 15–25% over the lifecycle of a tokenized fund compared to a traditionally administered equivalent.

Liquidity premium and asset value appreciation. Higher liquidity is associated with higher valuations across virtually every asset class. The 30% valuation increase observed in the St. Regis Aspen tokens within 18 months of issuance is consistent with the liquidity premium theory. As secondary markets deepen, this effect should become more pronounced and more reliable.

INSTITUTIONAL INVESTOR ADVANTAGES

Portfolio granularity: build precise allocations across dozens of properties without full asset purchases

24/7 settlement capability and dramatically shorter transaction cycles vs. traditional real estate

Programmable distributions: automated rent and interest payments directly to wallets

Use as on-chain collateral in financing transactions (repo, secured lending)

Transparent, auditable cap tables and transaction history on-chain

Access to previously closed private fund structures at lower minimums (KKR, Hamilton Lane)

RETAIL & HIGH-NET-WORTH ADVANTAGES

Fractional ownership of trophy and institutional-grade properties previously inaccessible

Entry at low minimums — from $50 on some platforms to $50,000 for semi-institutional offerings

Daily, weekly, or monthly income distributions automated by smart contract

Geographic diversification: own slices of properties across multiple countries

Potential secondary market trading where available, improving exit flexibility

Transparency of underlying asset: blockchain records provide real-time visibility

The Efficiency Gain That Is Frequently Underestimated

Most commentary on tokenization focuses on democratization, the retail access story. What is frequently underestimated is the pure operational efficiency gain for institutional participants. Traditional real estate settlement routinely takes 30–90 days. Traditional fund administration requires armies of accountants, transfer agents, and compliance officers. Tokenized structures can compress settlement to minutes and automate the bulk of fund administration through smart contracts.

J.P. Morgan's Onyx platform, which has processed over $900 billion in transactions, exists precisely because this efficiency gain is real and measurable at institutional scale. For institutions that deploy hundreds of billions across portfolios including real estate, even a modest improvement in settlement efficiency, collateral utilization, and administrative overhead translates to material economic benefit. BCG estimates potential cost savings of 35–65% in transaction and administration costs for tokenized versus traditionally managed real estate structures.

The Risks, Pitfalls, and Hard Lessons

RISKS & PITFALLS

The failures of 2025 were instructive. A series of tokenized real estate projects ran into difficulties that were not primarily technical — they were governance, legal, and architectural failures driven by insufficient attention to the hard work that separates a genuine tokenized investment vehicle from a token with a building's photograph attached to it. Below are a consistent set of risks that any serious participant must understand.

Regulatory & Securities Compliance Risk

In the U.S., most tokenized real estate offerings are securities under the Howey test — they represent investment contracts in which investors expect profits from others' efforts. Failure to comply with SEC Reg D, Reg S, or registered securities requirements has resulted in enforcement actions, disgorgement, and platform shutdowns. Internationally, the patchwork of securities laws, MiFID II in Europe, MAS in Singapore, SFC in Hong Kong and ADGM/DIFC in the Gulf, creates genuine cross-jurisdictional complexity. A multi-national tokenized transaction that fails to account for transfer restrictions by investor domicile has triggered regulatory flags that froze assets and exposed issuers to significant liability.

The Broken Link: Token vs Legal Rights

Perhaps the most consequential risk in current tokenized real estate: a broken link between the digital token and the legal ownership claim it purports to represent. If the smart contract does not programmatically enforce the rights described in the legal prospectus, the token holds no real-world value. In at least one high-profile 2025 case, token holders discovered that local land registries did not recognize the blockchain as a source of truth leaving them with a valid token and no legal claim on the building. Due diligence on the legal architecture, not just the technology stack, is essential.

Smart Contract & Technical Vulnerabilities

Smart contracts are immutable once deployed, which means a coding flaw can be permanent in its consequences. In October 2025, a major tokenized property platform lost $12 million to a reentrancy attack despite three prior security audits. The broader crypto ecosystem saw approximately $1.7 billion stolen from platforms in 2023. Every integration point in a tokenized system (oracles, cross-chain bridges, custody wallets) introduces potential failure modes. Ongoing audits, multi-signature custody, and bug bounty programs are minimum requirements, not optional enhancements.

Secondary Market Liquidity Illusion

Tokenization enables liquidity, it does not guarantee it. As of 2026, most real estate tokens trade primarily or exclusively on the platform that issued them, with thin secondary markets and limited interoperability across exchanges. KPMG, EY, and Deloitte have all flagged scarce secondary markets as the primary barrier to mainstream adoption. During market stress, the ability to find a buyer for a fractional token in a specific property in a specific market may be no better than traditional real estate and investors who believed otherwise have been disappointed. The liquidity premium is a future value proposition; it is not, in most cases, a current reality.

Valuation Opacity & Pricing Complexity

Real estate valuation is inherently subjective and infrequent. Unlike listed securities, there is no continuous price discovery mechanism for most tokenized property assets. The market price of a token can diverge significantly from the appraised value of the underlying asset in either direction, driven by platform-specific supply/demand dynamics, investor sentiment, and liquidity conditions that may have nothing to do with the fundamental value of the property. Standardized valuation models for tokenized real estate are only beginning to emerge.

Custody & Key Management Risk

Private key compromise results in permanent, irreversible loss of tokenized holdings with no traditional recovery mechanism available. Unlike a lost stock certificate (replaceable) or a frozen bank account (recoverable through legal process), lost private keys for self-custodied real estate tokens are typically unrecoverable. The choice of custody model — self-custody, qualified custodian, multi-signature — is one of the most consequential decisions in any tokenized real estate program. Platform insolvency adds a further dimension: if the issuing platform fails, token holders' claims may be subordinated to other creditors in ways that are still being tested in bankruptcy courts.

Tax Complexity & Cross-Border Frictions

Tokenized real estate transactions often involve issuers and investors in multiple jurisdictions, each with different tax treatment of digital assets, capital gains, and rental income. U.S. federal withholding requirements mandate that issuers withhold 30% of proceeds from offshore investors in many structures. GDPR's "right to erasure" conflicts with blockchain's immutability for European investor data. The aggregation of these frictions adds real cost and complexity to cross-border tokenized real estate structures, often underestimated in initial structuring.

Fraud, Misrepresentation & Platform Risk

The low barriers to entry for launching a tokenization platform have created opportunities for fraudulent or misleading offerings. Self-regulation in the absence of enforceable auditing requirements has proven insufficient in multiple documented cases. Investors must demand clear disclosure of valuation methodologies, redemption terms, dispute resolution processes, fee structures, and the identity and track record of property managers and platform operators. The presence of a blockchain does not confer legitimacy on a poorly structured or dishonestly marketed offering.

Three Vectors Capital - Practitioner Note

The most dangerous moment in any tokenized real estate transaction is when the technology appears to be working and the legal architecture has not been stress-tested. Compliance-by-design — embedding AML, KYC, investor eligibility, transfer restrictions, and jurisdictional rules directly into the smart contract layer is the minimum standard for institutional-grade tokenization. Projects that treat compliance as a post-launch plugin rather than a foundational architectural requirement face disproportionate legal and reputational exposure.

The gap between what the technology can do and what the legal and regulatory framework permits is consistently larger, more expensive to bridge, and more consequential than most issuers anticipate. Engaging experienced advisors before the first line of code is written is not optional — it is the difference between a successful capital raise and a regulatory enforcement action.

The Trajectory: From Billions to Trillions

Multiple independent analyses converge on the same broad conclusion: tokenized real estate will grow from a $300 billion market in 2024 to somewhere between $2 trillion and $4+ trillion by the mid-2030s. The variance in estimates reflects different assumptions about regulatory progress, secondary market development, and the pace of institutional adoption not disagreement about the direction of travel.

Gartner's 2024 Hype Cycle for Web3 and Blockchain classifies tokenization as an "adolescent technology" and projects mainstream adoption within 2–5 years from that assessment. The BCG-Ripple 2025 report projects the entire tokenized RWA market growing from $0.6 trillion to $18.9 trillion by 2033, a CAGR of 53%, with real estate as a primary contributor.

What Comes Next: The Conditions for Scale

FORWARD OUTLOOK

The tokenized real estate market is not a question of if — it is a question of pace and precondition. Several conditions must be met for the market to achieve its multi-trillion-dollar potential, and each of these conditions is in various stages of development.

Secondary market depth is the critical unlock. The single most important constraint on broader adoption for both retail and institutional investors is the thinness of secondary markets. Tokens locked to a single issuance platform with no interoperability are not meaningfully more liquid than a traditional real estate investment. The Swift/Chainlink cross-network transfer initiative, the EU's broader MiCA framework for digital asset service providers, and the emergence of regulated alternative trading systems (ATS) in the U.S. are all working toward this unlock. When true secondary liquidity arrives, tokens tradeable across multiple regulated venues with real price discovery, the liquidity premium embedded in tokenized assets will become measurable and real.

Regulatory harmonization will determine geographic concentration. Markets with clear, permissive, and predictable regulatory frameworks like Singapore, UAE, Hong Kong and Luxembourg, and increasingly the U.S. under the current administration, will attract disproportionate deal flow. Markets with hostile or uncertain regulation will see capital and talent flow elsewhere. Issuers structuring tokenized real estate should expect their jurisdiction of choice to significantly affect their achievable investor base and ultimate deal economics.

AI integration will transform asset management. Several leading platforms are already embedding AI-driven compliance, automated valuation, and real-time portfolio monitoring into their tokenization infrastructure. Zoniqx's AI-driven compliance framework and DigiShares' planned AI valuation tools represent early iterations of what will become standard infrastructure. Over the next five years, the combination of on-chain transaction data, AI-driven analytics, and automated compliance will create a level of portfolio transparency and operational efficiency in real estate investment that traditional structures cannot match.

Tokenized REITs represent a probable convergence. Traditional REITs, currently required to distribute 90% of taxable income to shareholders and bound by rigid governance structures, are increasingly exploring tokenization as a way to offer more flexible, accessible, and liquid investment products. A tokenized REIT structure could combine the regulatory familiarity of a REIT with the programmability, fractional accessibility, and secondary market tradability of a token. This convergence, if it materializes at scale, would be the single largest catalyst for mainstream retail participation in tokenized real estate.

Three Vectors Capital advises asset owners, issuers, and investors across the digital assets and real estate sectors.